OpenMx Structural Equation Modeling

rranne2@uic.edu

Joined: 12/10/2018

rranne2@uic.edu

Joined: 12/10/2018

latent difference score issues

Hello,

- Read more about latent difference score issues

- 3 comments

- Log in or register to post comments

blazej

Joined: 11/20/2018

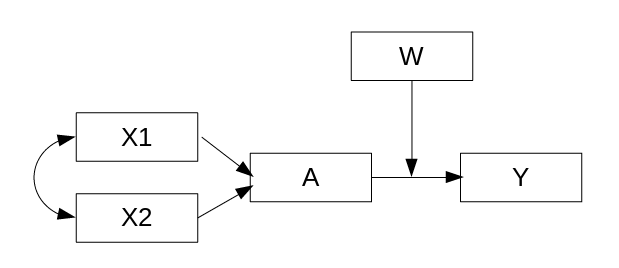

Looking for help with including a moderator to a path model

Greetings,

this is my 1st post, so please forgive me if this is offtopic.

In sort of new to SEM / modelling in general. So far I managed to make some sense of lavaan() syntax in R, to run a path model like this (file attached).

Before introducing the W moderator (continuous) this model was specified (in lavaan) as:

model <- '

X1 ~~ X2

A ~ X1 + X2

Y ~ A'

All variables are observed and continuous.

Julia

Joined: 03/29/2012

Julia

Joined: 03/29/2012

Parameter contraints across subgroups

Hi all,

- Read more about Parameter contraints across subgroups

- 3 comments

- Log in or register to post comments

paulT

Joined: 11/03/2017

paulT

Joined: 11/03/2017

Empirical Underidentification with a bifactor type model

First post by new user: Can anyone give some advice on an empirical under-identification issue please? I am trying to fit the following model:

resVars <- mxPath( from=mylabels, arrows=2,

free=TRUE, values=rep(1,12),

labelatVars <- mxPath( from=c("X1","X2"), arrows=2, connect="unique.pairs",

free=c(TRUE,FALSE,TRUE), values=c(1,0,1), labels=c("varX1","cov","varX2") )

cjcook

Joined: 05/22/2017

LISREL Simulation

Hello,

I am trying to simulate data using the endogenous variables only LISREL model as seen on page 133 of the OpenMx.pdf help documentation. I was able to simulate data from a state space model using the example in the help documentation on page 174. Now I am modifying that piece of code for a LISREL model. However I am running into an error. Below is my code.

- Read more about LISREL Simulation

- 4 comments

- Log in or register to post comments

Soyoung

Joined: 05/08/2017

Soyoung

Joined: 05/08/2017

multilevel path/structural equation models in OpenMx

Hi,

Is it possible to estimate multilevel path/structural equation models with OpenMx?

If it is possible, is there an example code for multilevel mediation (path) model?

Attached files are the example of multilevel path model using Mplus.

Source: Heck, R. H., & Thomas, S. L. (2015). An introduction to multilevel modeling techniques: MLM and SEM approaches using Mplus. Routledge.

Hope I can do the same analysis using OpenMx.

Thank you in advance.

Soyoung.

iloo

Joined: 05/26/2010

iloo

Joined: 05/26/2010

Optimization issues - binary with low prevalence

Hey,

I work with OpenMx using a bit different data than most others; often data comes from a full population and has quite many rows (up to 3 million). A common type of analysis is for relatives with one or more binary variables, e.g. observed disease diagnosis, where the prevalence is low, e.g. 1% to 0.05%. The complexity of the models vary from simple 2x2 covariance matrices without any definition variables to 8x8 covariance matrices with several definition variables adjusting the means/thresholds.

IvanVoronin

Joined: 08/18/2013

Wierd estimate of mean in a simple model

Dear all,

I've met a weird issue with means running a simple model.

The data:

Cov<-matrix(

c(10,3.0,6.5,

3.0,10,6.5,

6.5,6.5,10),ncol=3,nrow=3)

library('mvtnorm')

data<-as.data.frame(rmvnorm(1000,mean=rep(100,3),sigma=Cov))

names(data)<-c('X','Y','Z')

The covariance matrix corresponds the model:

X -> Z = 0.5

Y -> Z = 0.5

X <-> Y = 3

X <-> X = 10

Y <-> Y = 10

Z <-> Z = 3.5

All means are 100

The model:

aModel<-mxModel(type='RAM',name='Phenotypic model',

manifestVars=c('X','Y','Z'),

mxPath(from=c('X','Y'),to='Z',connect='single',

- Read more about Wierd estimate of mean in a simple model

- 1 comment

- Log in or register to post comments

rabil

Joined: 01/14/2010

rabil

Joined: 01/14/2010

Interpreting Output from mxTryHardOrdinal

The output below says a solution was found, but was it?

Begin fit attempt 21 of at maximum 21 tries

- Read more about Interpreting Output from mxTryHardOrdinal

- 2 comments

- Log in or register to post comments

rabil

Joined: 01/14/2010

Constrain Total Variance instead of Residual Variance in Ordinal Threshold Path Mdel

The path specification for an ordinal model in the documentation constrains the residual variances for the ordinal variables to 1. I would like to instead constrain the total variance for the ordinal variables to 1. But I'm not sure how to accomplish this. When the total variance is constrained to 1, there residual variance is constrained to 1 minus the factor loading squared (the factor loadings are constrained to be between -1 and 1) as I understand it.