| Attachment | Size |

|---|---|

| 26.42 KB |

{kind=link}

Dear Mike,

A colleague and I studied the factor structure of a scale using the metaSEM package. The reviewers asked us for residual covariance matrice of structural model we construct. I couldn't see a command for this in the metaSEM package. There is vcov but this command gives sampling covariance matrices. Is there a way to see residual covariance matrices?

Sincerely

The script that we used to construct our model is ad follow:

library(metaSEM)

library(lavaan)

sdeğ <- 6

değad <- c("m1","m2","m3","m4","m5","m6")

etiket <- list(değad,değad)

korver <- list()

for (i in 1:nrow(veri)){

korver[[i]] <- vec2symMat(as.matrix(veri[i,3:17]),diag = FALSE)

dimnames(korver[[i]]) <- etiket

}

korver

REM1 <- tssem1(Cov=korver, n=veri$N, method="REM", RE.type="Diag")

summary(REM1)

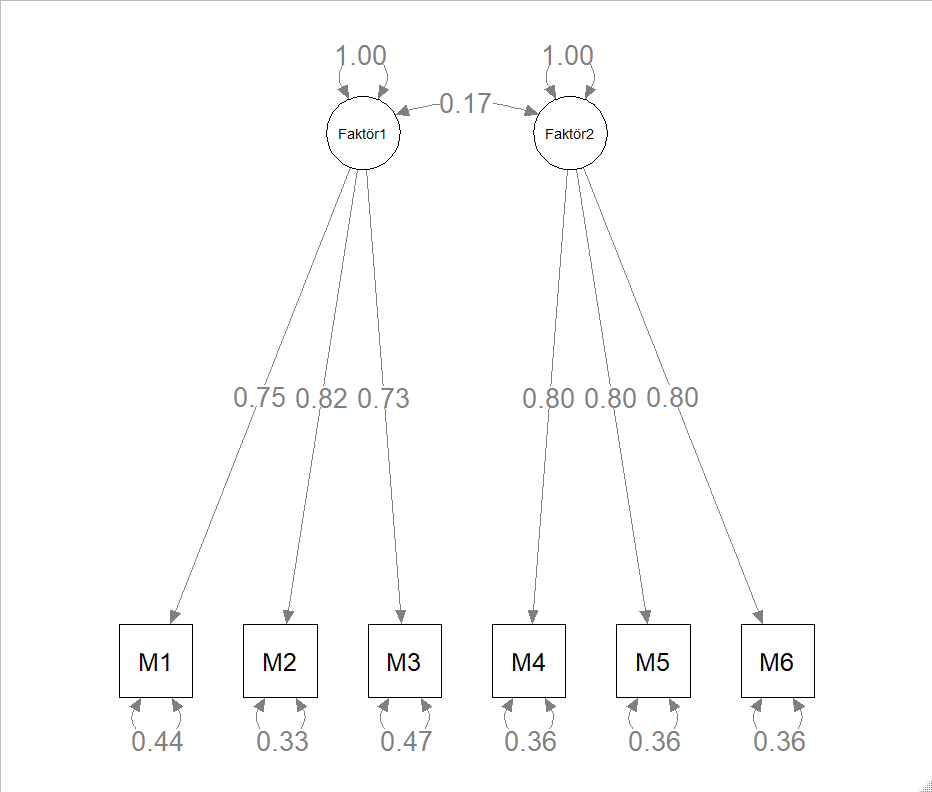

model<-"

Faktor1=~M1+M2+M3

Faktor2=~M4+M5+M6

Faktor1~~Faktor2"

RAM <- lavaan2RAM(model, obs.variables=c("M1","M2","M3","M4","M5", "M6"),

A.notation="on", S.notation="with")

REM2 <- tssem2(REM1, RAM=RAM, intervals="LB")

summary(REM2)

Call:

wls(Cov = pooledS, aCov = aCov, n = tssem1.obj$total.n, RAM = RAM,

Amatrix = Amatrix, Smatrix = Smatrix, Fmatrix = Fmatrix,

diag.constraints = diag.constraints, cor.analysis = cor.analysis,

intervals.type = intervals.type, mx.algebras = mx.algebras,

model.name = model.name, suppressWarnings = suppressWarnings,

silent = silent, run = run)

95% confidence intervals: Likelihood-based statistic

Coefficients:

Estimate Std.Error lbound ubound z value Pr(>|z|)

M1onFaktor1 0.75023 NA 0.69404 0.80902 NA NA

M2onFaktor1 0.81600 NA 0.75594 0.87878 NA NA

M3onFaktor1 0.72925 NA 0.67467 0.78664 NA NA

M4onFaktor2 0.79731 NA 0.72519 0.87357 NA NA

M5onFaktor2 0.80009 NA 0.72521 0.87772 NA NA

M6onFaktor2 0.79901 NA 0.72891 0.87430 NA NA

Faktor1withFaktor2 0.17314 NA 0.13774 0.20912 NA NA

Goodness-of-fit indices:

Value

Sample size 5769.0000

Chi-square of target model 11.0801

DF of target model 8.0000

p value of target model 0.1972

Number of constraints imposed on "Smatrix" 0.0000

DF manually adjusted 0.0000

Chi-square of independence model 2034.0182

DF of independence model 15.0000

RMSEA 0.0082

RMSEA lower 95% CI 0.0000

RMSEA upper 95% CI 0.0186

SRMR 0.0193

TLI 0.9971

CFI 0.9985

AIC -4.9199

BIC -58.2020

OpenMx status1: 0 ("0" or "1": The optimization is considered fine.

Other values indicate problems.)

plot(REM2)